The market move observed so far may therefore represent only the first stage of a much larger repricing. Put another way, gold has a flight path.

Submitted by Vince Lanci

The next phase may look very different. If the global adjustment to the dollar system begins feeding back into domestic financial markets, the Federal Reserve could face an increasingly difficult choice between maintaining interest rate control and maintaining financial stability.

In that environment gold begins functioning less like a commodity and more like a balance-sheet clearing asset within the global monetary system. The market move observed so far may therefore represent only the first stage of a much larger repricing. Put another way, gold has a flight path.

Just The Beginning

Gold, Currency Instability, and the Structure of the Next Monetary Phase

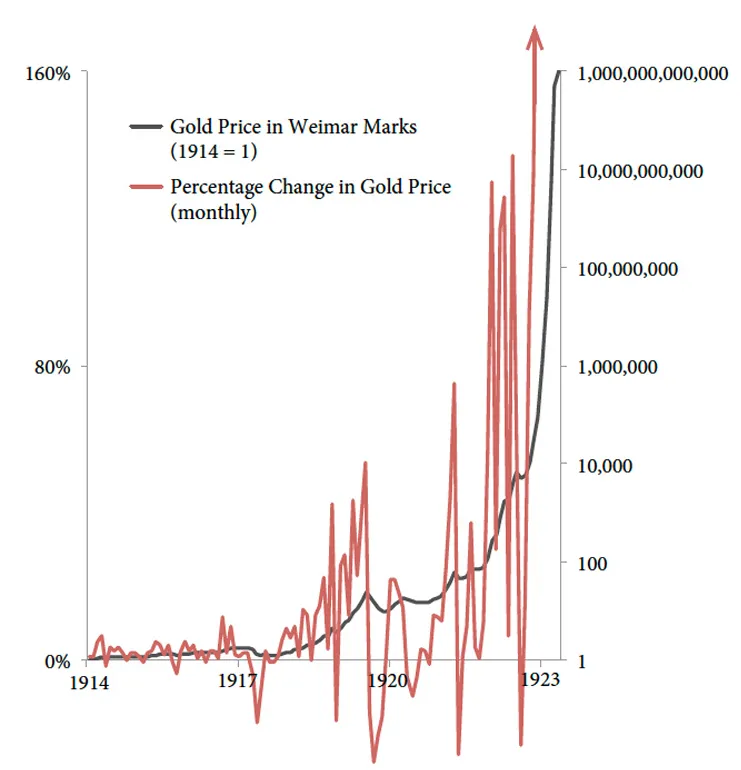

The February 2026 research letter from Myrmikan Research examines the structural forces behind the current gold bull market and places them within a broader historical framework of currency crises. The central argument is that currencies rarely decline gradually. Instead, they tend to operate in unstable equilibrium until debt dynamics force a sudden repricing.

“Currencies do not usually fade; they tend to collapse.”

We would add also pointedly add that the tipping point concept applies quite well with currencies as they work until people stop believing in them… and they tend to stop believing all at once.

Currency systems function as the settlement layer for accumulated debt. When debt expands faster than the productive capacity of the economy, the monetary unit becomes the mechanism through which the imbalance is resolved. In practice this means the currency absorbs the adjustment that balance sheets cannot.

The mechanism typically begins with rising leverage across the economic system. Governments, corporations, and households expand borrowing either in anticipation of future debasement or simply to sustain spending in an inflationary environment. As the stock of debt grows, the demand for liquidity required to service that debt expands alongside it.

Central banks attempt to maintain equilibrium by expanding the money supply just enough to support interest payments while avoiding an outright collapse in the currency. This balancing act can persist for years. Eventually, however, a shock disrupts the system. When debt servicing falters, policymakers confront the risk of deflation and typically respond with rapid monetary expansion or currency devaluation.

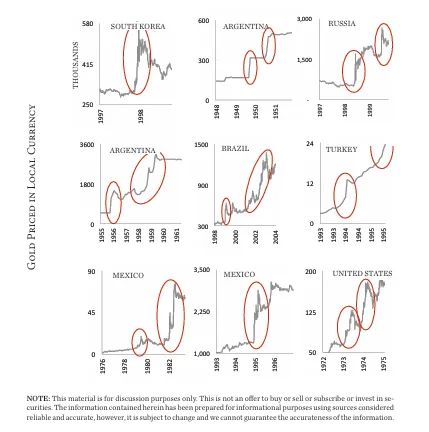

Historical Pattern of Currency Breakdowns

The report illustrates this dynamic through historical episodes where gold prices surged in local currency terms during periods of monetary instability. Examples include Argentina, Brazil, Turkey, Mexico, South Korea, Russia, and the United States during inflationary episodes. In each case, gold’s move accelerated sharply once confidence in the currency weakened.

As debt cycles repeat, markets begin to anticipate future devaluations. Expectations evolve from the likelihood of debasement to the speed at which debasement may occur.

“The market starts to guess how fast the debasement will be; then it anticipates by how much the debasement will accelerate.”

Currency crises rarely unfold linearly. Markets initially price policy mistakes. Eventually they begin pricing the reaction function of policymakers themselves. When investors begin anticipating how central banks will respond to instability rather than focusing on the instability itself, volatility increases dramatically. Gold often becomes the transmission mechanism for that shift.

The Current Gold Bull Market

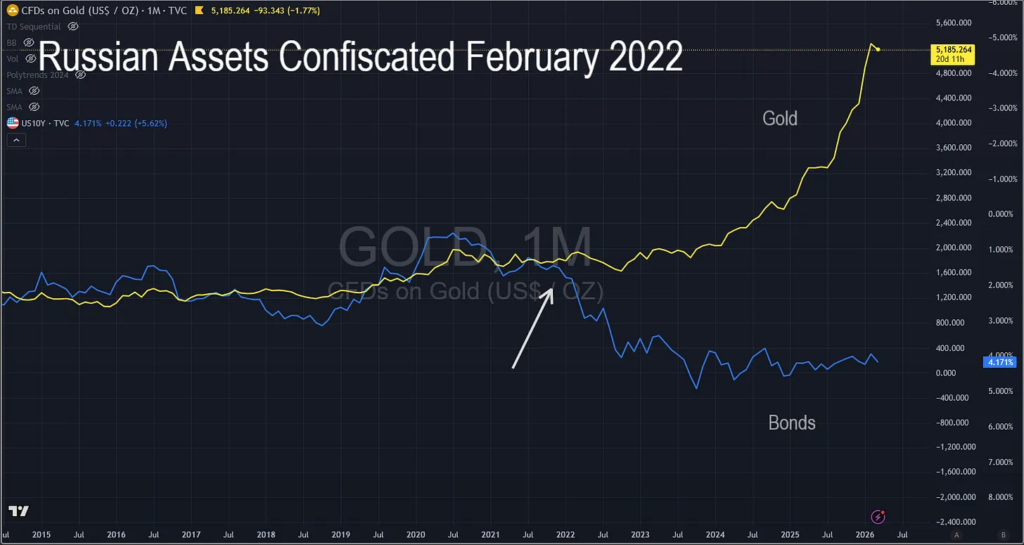

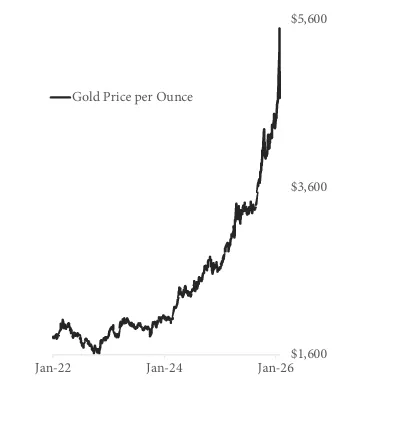

The report argues that the present gold bull market differs from historical currency collapses because it began outside the domestic financial system. The turning point occurred in February 2022 when the United States froze Russia’s dollar reserves following the invasion of Ukraine.

“Central banks… began to tip toe slowly out of the U.S. Treasury bond complex and into gold.”

The freezing of sovereign reserves fundamentally altered how many governments view the global monetary system. Dollar assets were no longer perceived purely as financial instruments; they became political instruments as well. In that environment gold regained an attribute it had largely lost during the post-Bretton Woods era: neutrality.

Unlike sovereign bonds, gold cannot be sanctioned, frozen, or politically conditioned within the international settlement system. That characteristic explains why central bank gold accumulation accelerated after 2022 even as interest rates were rising.

The early stage of the bull market remained largely hidden behind the Federal Reserve’s tightening cycle. Higher interest rates typically pressure gold prices, and the metal initially declined. However, gold soon stabilized and began rising despite the tightening environment.

The report interprets this divergence as the beginning of the current bull market. From late 2022 through early 2026 the price of gold in U.S. dollars followed a steadily accelerating trajectory.

Importantly, the typical catalysts associated with currency crises have not yet appeared. There have been no widespread banking failures, no collapse in Treasury markets, and no forced monetization of government debt.

“There are none of the normal crises that send a currency suddenly lower. They will come.”

The Dollar’s International Position

The report frames the challenge to the dollar primarily as an international issue rather than a domestic one. The dollar remains the dominant reserve currency largely by default, yet dissatisfaction with the current system has grown among major geopolitical actors, including Russia, China, and other BRICS nations.

For decades, global demand for dollar assets allowed the United States to finance persistent deficits through foreign capital inflows. This structure effectively enabled the United States to run what Jacques Rueff famously called “a deficit without tears.”

However, if foreign capital begins reducing exposure to dollar assets, the adjustment mechanism changes. Instead of international savings financing U.S. deficits, domestic financial markets must absorb the increased supply of government debt. The resulting pressure would likely appear first in leveraged sectors such as private equity and private credit.

Federal Reserve Policy Constraints

The report also examines the modern structure of Federal Reserve policy tools. Before the 2008 financial crisis, interest rates were largely controlled through reserve scarcity in the banking system. After quantitative easing flooded the system with liquidity, the Fed adopted a different framework.

Today the central bank manages interest rates primarily through Interest on Bank Reserves (IORB), paying banks interest on deposits held at the Fed. In theory this establishes a floor under market rates without requiring the Fed to shrink or expand its balance sheet.

In practice the system introduces new constraints. Paying interest on reserves requires continuous monetary expansion, particularly when the rate paid to banks exceeds the yield earned on the Fed’s bond portfolio. Since 2022 this mechanism has contributed to substantial operating losses at the central bank.

Reserves are also unevenly distributed across the banking system. Large institutions hold the majority of excess reserves, meaning the appearance of ample liquidity can mask localized shortages.

In December 2025 the Federal Reserve announced reserve management purchases to maintain liquidity.

“Reserve balances have declined to ample levels.”

In the language of central banking, “ample” often means reserves are approaching scarcity.

The Next Phases of the Gold Bull Market

The report outlines a three-phase framework for the gold market.

Phase One is the current stage, defined by international diversification away from dollar reserves.

Phase Two would emerge if domestic monetary expansion accelerates in response to financial stress. If newly created liquidity remains within the United States rather than circulating globally, inflationary pressures could intensify.

Phase Three would involve a sovereign debt spiral. Rising interest rates increase government debt servicing costs, expanding deficits and forcing additional Treasury issuance. Higher supply pushes yields higher, reinforcing the cycle.

At that stage policymakers may face a familiar historical choice between sovereign default and large-scale monetization of government debt.

Gold and Central Bank Balance Sheets

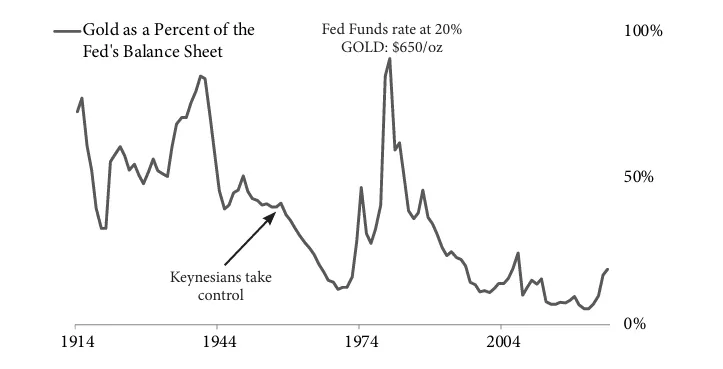

The report estimates potential gold prices by examining historical relationships between central bank balance sheets and gold reserves. Historically, gold represented roughly one-third to one-half of central bank reserves.

Applied to the current Federal Reserve balance sheet, this ratio implies a gold price between $8,395 and $12,595 per ounce.

“Gold is free market money and… its end goal is to balance balance sheets.”

In this framework gold functions less like a commodity and more like a clearing asset within the monetary system. When the existing structure of liabilities and reserves becomes unstable, gold prices adjust until balance sheets stabilize.

About the Author