Official Buying Survives Its First Major Stress Test as CBs Continue to Raise the Floor Under Gold

By Vince Lanci, GoldFix:

A Broader Buyer Base Emerges— The key lesson from the UBS report is not that central banks are driving gold higher. Rather, the feared collapse in official demand never materialized.

Raising the Floor: More and Different Central Banks Still Buying Gold

Official demand remains strong, but UBS argues investors, not central banks, still determine where gold trades next on a day to day basis

“Central banks may not be pushing gold higher, but they continue to make it harder for gold to fall.”

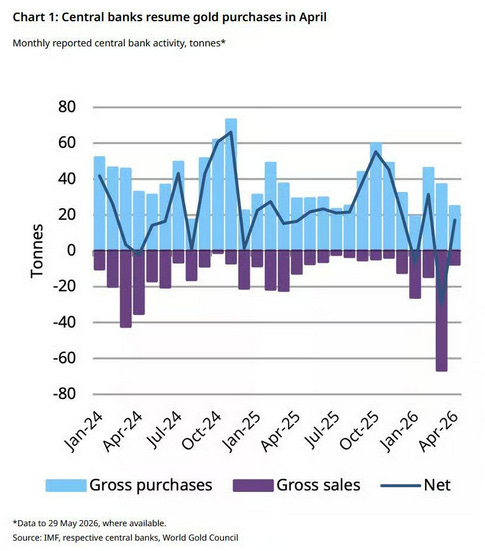

For much of 2026, one of the biggest concerns hanging over the gold market was the possibility that central banks had quietly shifted from buyers to sellers. Rising geopolitical tensions, a stronger U.S. dollar, higher real interest rates, and concerns surrounding Middle Eastern reserve management all fueled speculation that official-sector gold accumulation might be coming to an end.

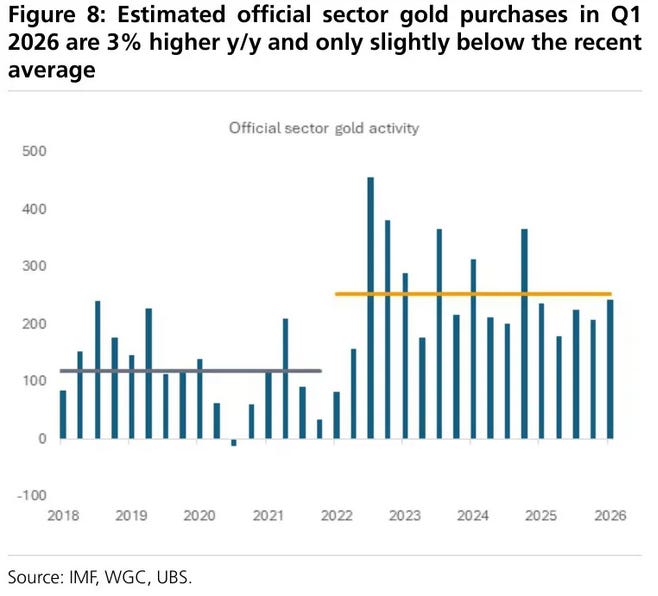

According to a new report from UBS strategist Joni Teves, those fears appear to have been overstated. World Gold Council data showed central banks and other official institutions purchased a net 244 tonnes of gold during the first quarter of 2026, a 3% increase from a year earlier and a figure that exceeded market expectations.

Official Buying Survives Its First Major Stress Test

The concern was understandable.

As conflict intensified in the Middle East, oil prices surged, inflation expectations rose, and investors began anticipating a more hawkish Federal Reserve response. Gold faced pressure from higher real yields and a stronger dollar, reviving traditional macro headwinds that often weigh on precious metals.

At the same time, rumors circulated that several central banks could be forced to liquidate portions of their gold reserves to defend currencies, support government finances, or raise dollar liquidity.

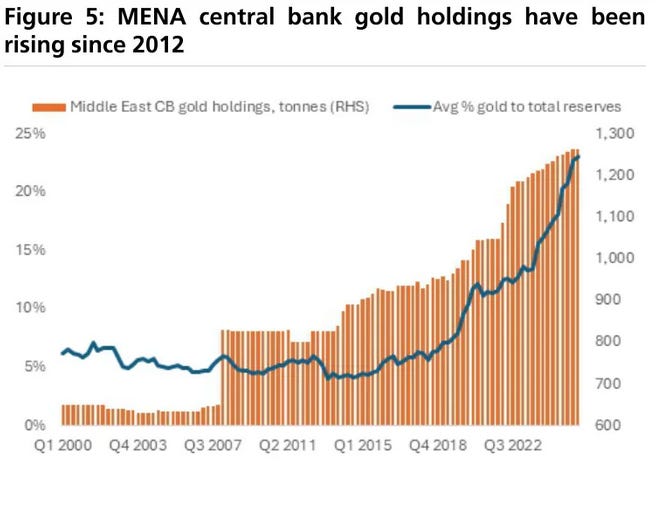

Türkiye became the focal point of those concerns after reports suggested the country’s central bank had reduced gold holdings by roughly 50 tonnes. Yet UBS argues the situation was likely more complicated than outright liquidation. Gold swaps, domestic liquidity operations, and commercial banking activity can all affect reported reserve levels without representing a true change in long-term reserve strategy.

“Headline reserve changes do not necessarily equal structural selling.”

Looking beyond Türkiye, the broader trend across emerging markets remains intact.

Gold’s Real Drivers Remain Investor Flows

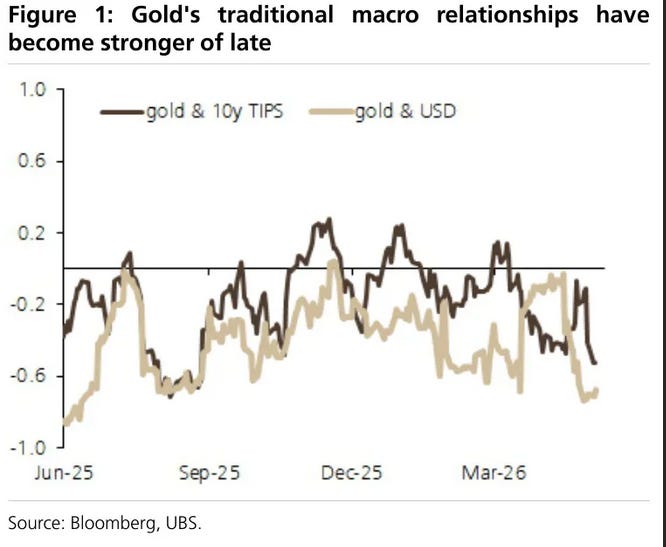

Perhaps the most important takeaway from the UBS analysis is the distinction between what supports gold and what actually drives it.

The report argues that official-sector purchases are often misunderstood. Central banks do not typically act as marginal price setters. Instead, short-term gold prices remain largely determined by investor positioning, real interest rates, and currency markets.

By steadily absorbing physical supply, reducing available liquidity, and maintaining a long-term accumulation strategy, official buyers create a structural foundation beneath the market.

In other words, central banks may not be responsible for gold’s rallies, but they increasingly appear responsible for limiting its declines.

A Broader Buyer Base Emerges

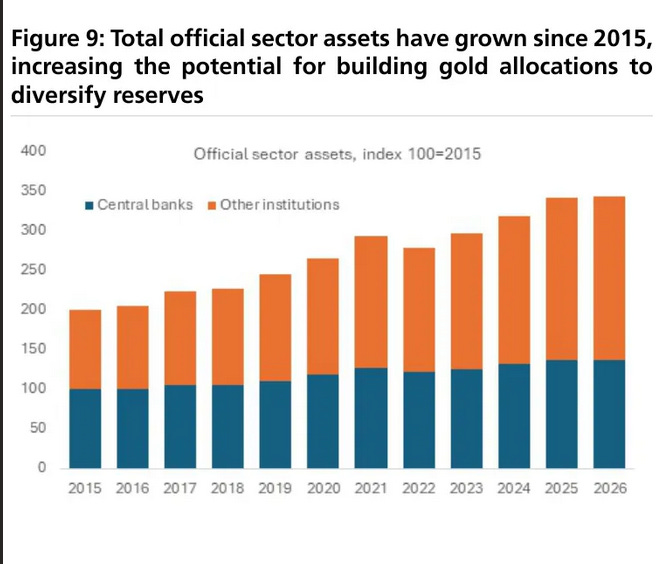

Another noteworthy development is the possibility that gold demand is expanding beyond the traditional group of large central-bank buyers.

UBS notes that some of the institutions most active during the past several years have slowed the pace of accumulation. However, new official-sector participants appear to be entering the market. Other sovereign institutions, reserve managers, and previously inactive buyers may now be stepping in as geopolitical fragmentation accelerates and reserve diversification becomes increasingly important.

That broadening participation helps explain why official demand has remained resilient despite record-high prices.

GoldFix Take

“The market spent months worrying about who might sell gold. The data suggest more institutions are still looking for reasons to buy it.”

The key lesson from the UBS report is not that central banks are driving gold higher. Rather, the feared collapse in official demand never materialized.

Gold continues to trade primarily on real rates, the dollar, and investor sentiment. Yet beneath those daily fluctuations sits a growing group of sovereign buyers willing to absorb supply and hold gold for strategic reasons rather than speculative ones.

As long as that foundation remains intact, periods of weakness may continue to look less like the start of a bear market and more like opportunities for long-term accumulation.