The quarter, ending September 30, 2025, highlighted the successful integration of the recently acquired Los Gatos Silver Mine and operational improvements across its portfolio, positioning the company for continued growth in a strengthening precious metals market.

Record Silver Output Drives Revenue Surge

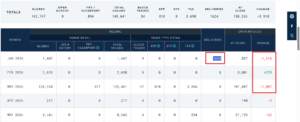

First Majestic reported consolidated revenue of $285.1 million for Q3 2025, marking a 95% increase year-over-year and reflecting the company’s expanded production capacity. This growth was fueled by a record silver production of 3.9 million ounces, a staggering 96% rise from the prior year, bringing year-to-date silver output to 11.3 million ounces.

Total silver equivalent (AgEq) production reached 7.7 million ounces, underscoring the contributions from key assets including San Dimas, Santa Elena, and the ramp-up at Los Gatos, where First Majestic holds a 70% interest following its January 2025 acquisition of Gatos Silver Inc. Earnings per share (EPS) came in at $0.07, missing the consensus forecast of $0.11 by 36%, primarily due to one-time integration expenses and lower-than-expected base metal contributions.

Despite the miss, CEO Keith Neumeyer described the results as “the best quarterly financial statement we have ever had in the company’s history” during the earnings call, emphasizing the operational momentum.

Many Analysts Are Predicting a Silver Move to $72-$75 in early 2026 if Silver Prices Break Through $55/oz to the Upside.

What are the Implications of $75/Oz Silver for Silver Producers Such as First Majestic Silver in 2026?

Looking ahead to Q1 2026, a silver price move to $75 per ounce could transform First Majestic’s financial trajectory, amplifying profitability amid stable production and costs. Assuming quarterly silver output mirrors Q3’s 3.9 million ounces (with AgEq at ~7.7 million, including gold at ~$3,000/oz equivalent), revenue from silver alone could exceed $292.5 million, up from ~$117 million at $30/oz, driving total quarterly revenue toward $500 million when factoring in by-product credits from gold, lead, and zinc.

With AISC holding at ~$21 per AgEq ounce, gross margins would balloon to over 70%, yielding EBITDA north of $300 million and free cash flow potentially surpassing $250 million—enough to accelerate exploration at high-potential sites like Navidad, fund aggressive buybacks, or eliminate remaining debt. This windfall would enhance dividend sustainability and shareholder returns, but risks such as cost inflation from labor or energy in a high-price environment, or operational disruptions, could temper gains; nonetheless, it underscores First Majestic’s leverage as the purest large-scale silver play among peers. First Majestic’s Q3 2025 performance solidifies its position as a premier silver producer, with operational excellence offsetting external headwinds.

As silver’s industrial and safe-haven demand intensifies, the company is well-poised for value creation in 2026 and beyond.

Investors should monitor Q4 results and exploration updates for further catalysts.

Disclaimer: This is not a recommendation to buy First Majestic Silver Corp. The author personally owns stock in First Majestic Silver Corp.

The above article is simply an analysis of how a hypothetical silver price increase could substantially impact silver producing companies.

Do your own due diligence, and invest accordingly.