100 oz Silver GIVEAWAY Ends TUESDAY!

Make Sure You’ve Subscribed to SilverTrade on Youtube to

Watch the LIVE DRAWING June 30th!

SilverTrade – YouTube

China’s RMB Internationalization via Gold Collateral

China is building the infrastructure to link RMB liquidity with gold liquidity through Hong Kong, the SGE, clearing, vaulting, and potential collateral use. Recent margin hikes may be pre-emptive risk control, discouraging leveraged speculation before gold becomes more financeable, repo-eligible, and central to RMB internationalization strategy. The margin hikes are merely preparation for the bigger event.

China’s Gold-RMB Architecture and the Emerging Collateral Question

Authored by Eric Yeung and Vince Lanci with contributions by Bai Xiaojun

Executive Overview

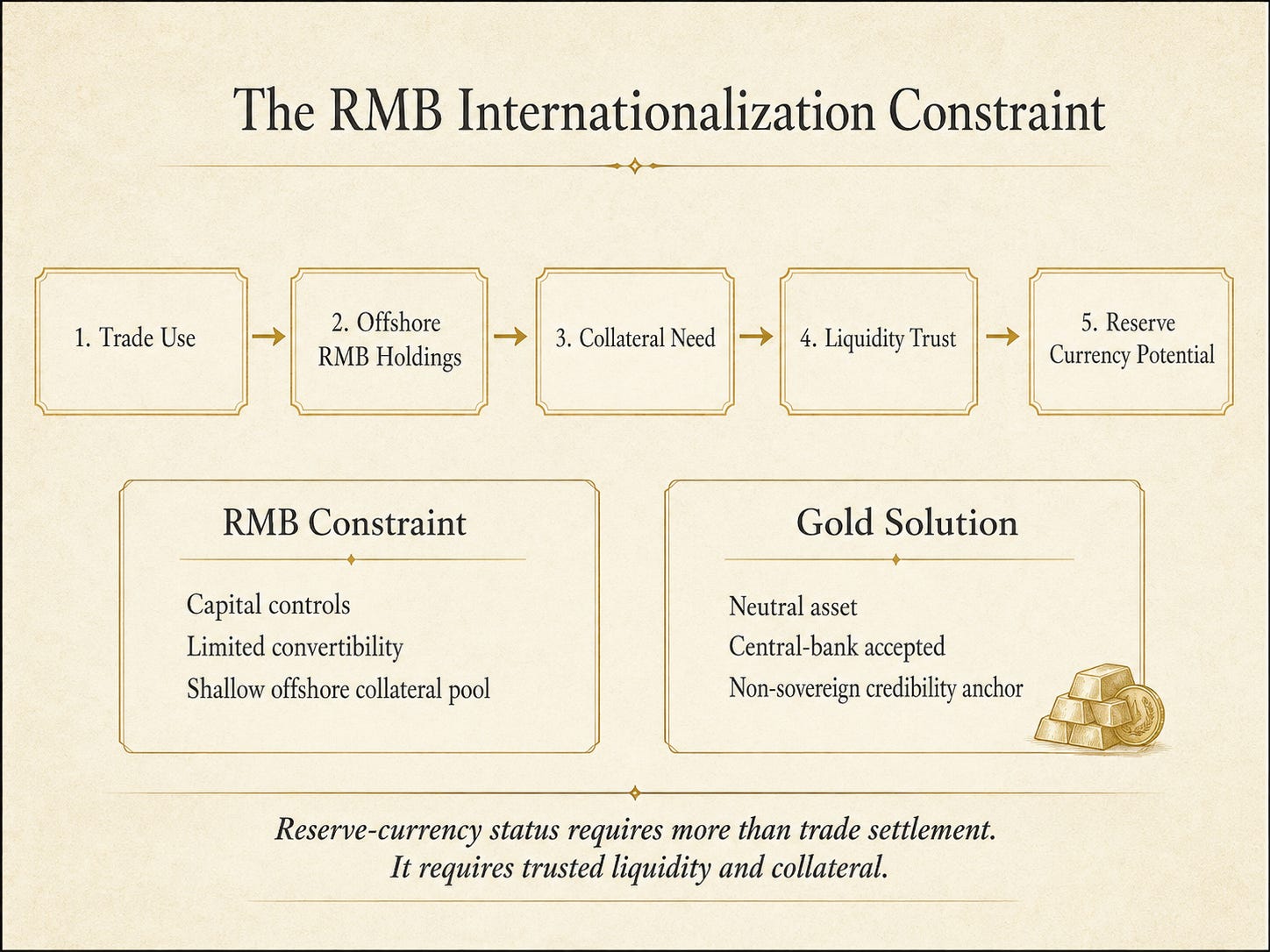

China’s effort to internationalize the RMB has often been analyzed through trade settlement, swap lines, bilateral payment systems, and the gradual development of offshore RMB markets. Those channels are important, but they do not fully address the central constraint facing any reserve-currency challenger: liquidity. A currency can be used for trade without becoming a reserve asset. To become a reserve asset, it must be supported by deep, trusted, and financeable instruments that foreign institutions can hold, pledge, borrow against, and convert under stress.

The thesis developed by Eric Yeung and Vincent Lanci is that China’s gold strategy should be understood inside that liquidity problem. The argument is not that China is preparing a simple gold-backed RMB in the classical sense. The argument is that China is attempting to build a gold-linked liquidity architecture around the RMB, using physical gold, clearing infrastructure, offshore vaulting, and eventually collateral treatment to make RMB balances more acceptable outside the mainland.

The latest developments in Chinese precious-metals margin policy and Hong Kong’s expected gold-clearing launch strengthen that framework. They do not prove that gold has been formally designated as high-quality liquid asset, or HQLA, collateral. They do, however, add another piece to a broader institutional pattern: China is building the market structure required for gold to move from reserve asset toward liquidity asset.

The RMB Internationalization Problem

The internationalization of a currency requires more than trade usage. Foreign holders need confidence that the currency can be deployed beyond bilateral settlement. The dollar’s strength rests not only on invoicing power, but on the depth of the Treasury market, the repo market, the derivatives system, and the global banking network that treats U.S. government debt as core collateral.

China has long sought to expand RMB use internationally, but the RMB faces structural limits. It is not fully convertible in the same manner as the dollar. China maintains capital controls. Foreign institutions remain cautious about holding large RMB balances without a deep offshore collateral ecosystem. As a result, RMB internationalization requires a mechanism that can reduce foreign-holder uncertainty.

Peter Schiff joined The SilverTrade Insider for a MUST WATCH interview breaking down The Fed’s threat to kill inflation & its impact on the gold & silver markets.

The legendary economist and market strategist warns that Keven Warsh is going to do the EXACT same thing as Powell, Yellen, Bernanke, & Greenspan and choose INFLATION over a complete collapse of the financial system! Schiff warns if The Fed doesn’t MONETIZE the debt, we’re going to have a WORSE FINANCIAL CRISIS than 2008!

Peter also goes OFF EXPOSING the gov’t FRAUD and CORRUPTION…but warns that even the US Gov’t won’t be able to stop what’s coming…

Gold provides one answer. It is widely held by central banks, accepted across political systems, and not the liability of a foreign sovereign issuer. For countries concerned about sanctions, reserve freezes, or dollar-system dependence, gold offers a neutral asset. The Yeung-Lanci thesis places gold at the center of China’s attempt to solve the RMB credibility problem.

Hong Kong, the SGE, and the Offshore Gold Channel

The expected launch of Hong Kong’s gold-clearing system in July is therefore significant. Reports have stated that Hong Kong is targeting a July launch for a government-owned gold-clearing system connected to the Shanghai Gold Exchange, with the city also planning to expand gold storage capacity to more than 2,000 tonnes within three years. Reuters previously reported that Hong Kong and the Shanghai Gold Exchange had agreed to develop a central gold-clearing system, strengthening Hong Kong’s role as an international bullion center.

The Shanghai Gold Exchange has already established offshore infrastructure in Hong Kong. In 2025, the SGE announced the launch of an International Board certified vault in Hong Kong, along with gold contracts deliverable in the city. That development matters because it places physical delivery, offshore vaulting, and RMB-linked gold trading inside a jurisdiction that connects mainland China to international capital.

The institutional logic is clear. A gold market that remains entirely domestic cannot serve as the foundation for international RMB liquidity. Gold must be tradable and deliverable both inside and outside China’s territory. Hong Kong provides the offshore legal, custody, and settlement environment

Margin Policy as Market-Structure Signal

The new margin increases on Chinese precious-metals deferred contracts are the latest development. Several Chinese banks reportedly raised margin requirements on personal gold and silver deferred SGE contracts, with some ratios moving as high as 140%. Reports also noted that margin requirements above 100% effectively eliminate leverage for individual traders, making speculative participation in these products far less attractive.

The timing is important. Margin increases are usually associated with rising volatility, speculative excess, or disorderly price appreciation. In this case, the increases followed a period of gold-price decline. That makes the move appear less like a conventional reaction to overheating and more like pre-emptive risk control.

**Breakout explanation footnoted1

The effect is straightforward. Retail traders are discouraged from participating in leveraged paper gold and silver SGE products. Fully funded exposure becomes more rational than leveraged deferred exposure. In practical terms, the policy pushes activity away from speculative paper trading and toward physical or fully margined exposure.

That does not prove that the margin hikes were ordered because of the Hong Kong launch. It does not prove that China is about to announce a formal gold-collateral regime. It does, however, align with the broader architecture. A system designed to support gold-linked RMB liquidity would benefit from lower speculative leverage, cleaner price formation, and a stronger physical-market foundation.

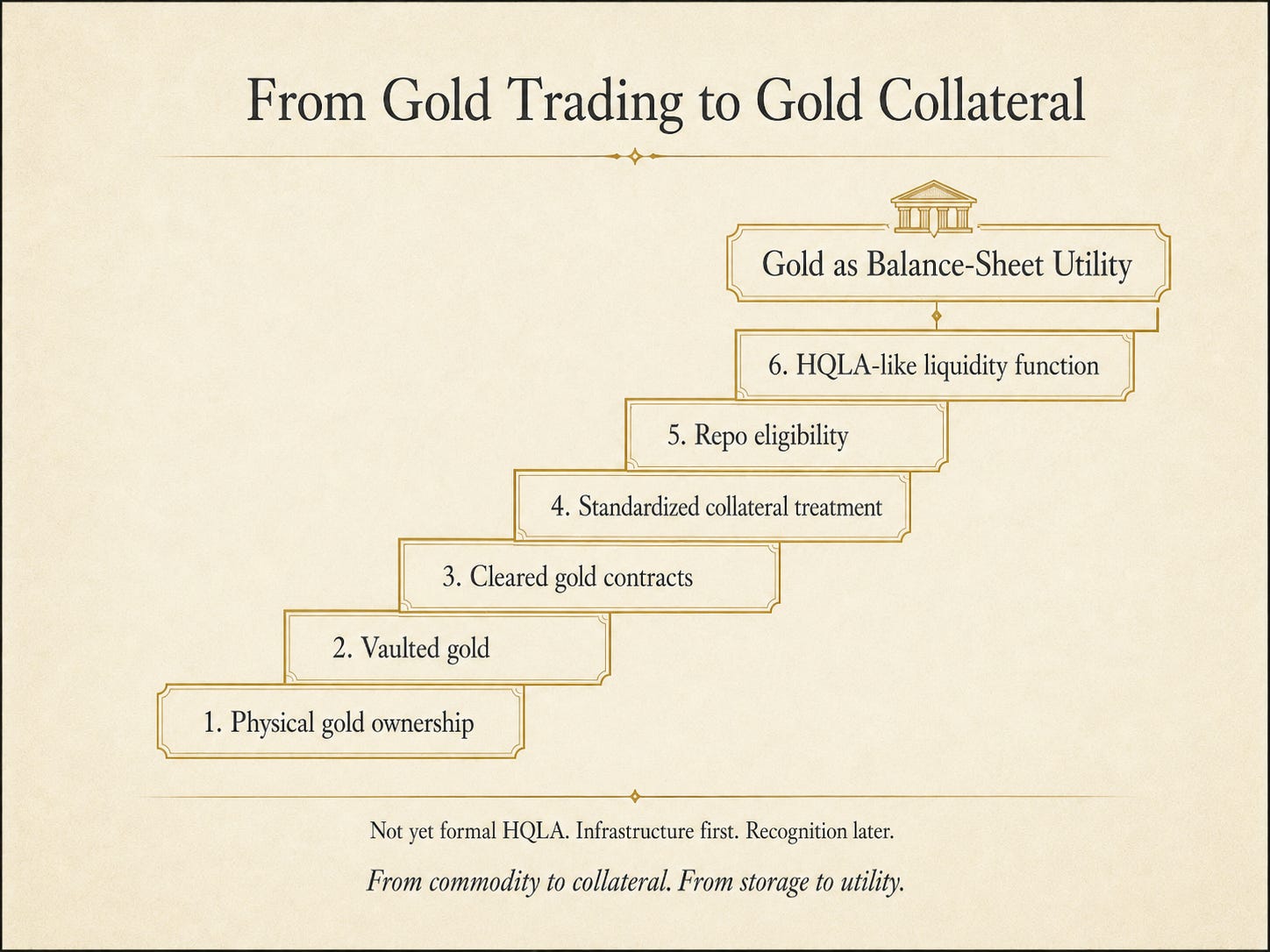

From Gold Trading to Gold Collateral

The central institutional question is whether gold remains a traded commodity or becomes a financeable collateral asset. Trading alone is insufficient for reserve-currency competition. A market can have active spot and futures trading without becoming a balance-sheet utility. For gold to support RMB internationalization, it must be capable of supporting borrowing, lending, repo, and settlement.

That requires infrastructure. It requires recognized vaults, title clarity, standardized contracts, reliable clearing, haircut schedules, liquidity rules, and bank balance-sheet treatment. The Hong Kong-SGE framework appears to be building several of those components. The missing step is formal regulatory recognition.

HQLA is a precise regulatory concept. It should not be used loosely. Under bank liquidity frameworks, HQLA treatment depends on eligibility, liquidity characteristics, valuation standards, and supervisory approval. At present, there is no publicly confirmed regulatory statement showing that China or Hong Kong has designated physical gold as formal HQLA collateral.

The more accurate formulation is that China is building infrastructure that could allow physical gold to become HQLA-like or repo-eligible inside an offshore RMB framework. That distinction matters. The thesis does not require an immediate public declaration that gold is HQLA. It requires gold to become sufficiently liquid, standardized, and financeable to support RMB balance-sheet usage.

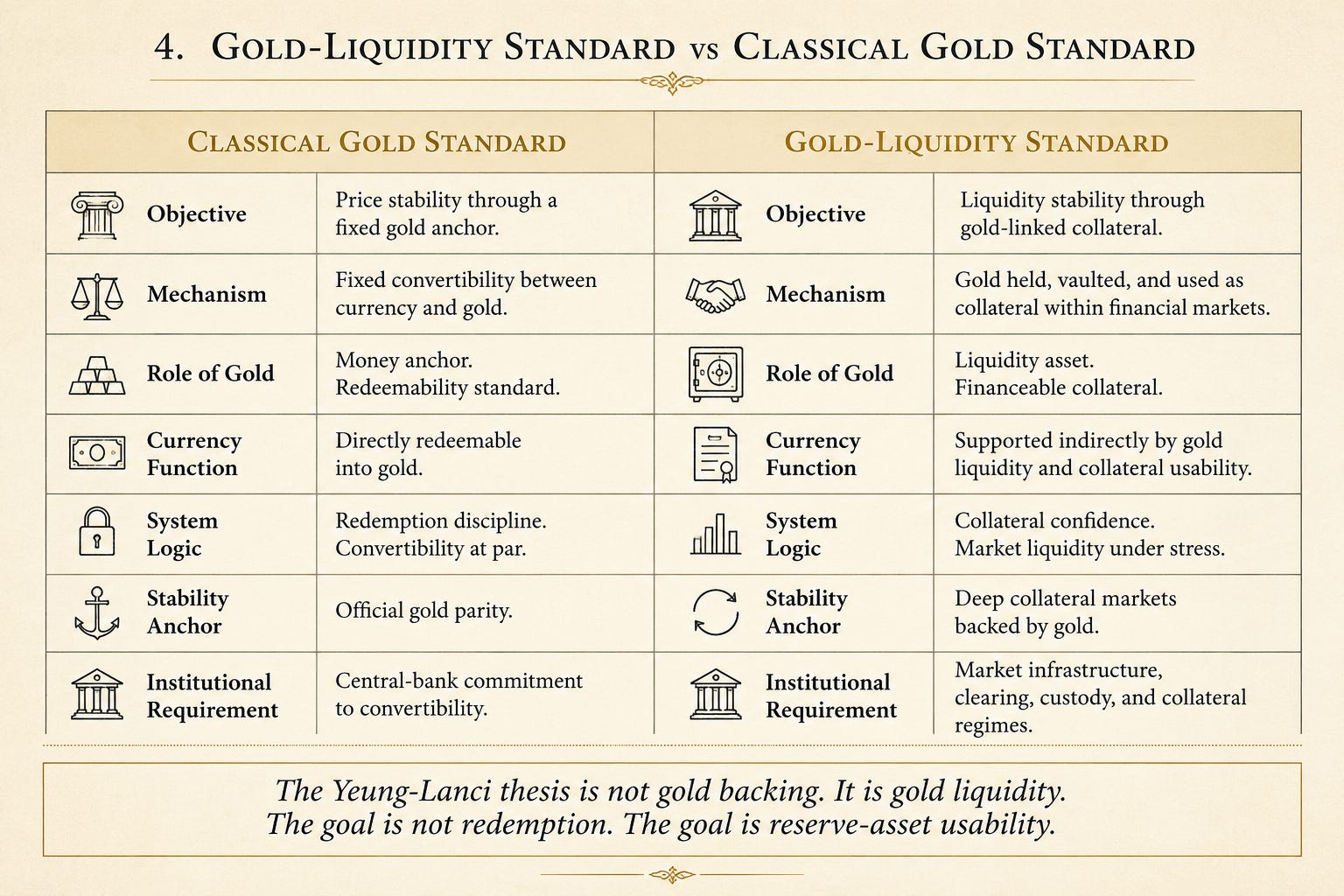

A Gold-Liquidity Standard, Not a Classical Gold Standard

The Yeung-Lanci thesis should not be confused with a claim that China will announce a traditional gold-backed RMB. A classical gold standard requires explicit convertibility at a fixed price. China’s likely path is more flexible and more institutional.

The more plausible model is a gold-liquidity standard. Foreign institutions holding RMB would not necessarily redeem currency directly into gold at a fixed official rate. Instead, they would operate inside a system where RMB balances are connected to gold contracts, gold vaulting, gold clearing, and potentially gold-backed financing. Gold would provide an exit, a collateral base, and a credibility anchor without requiring a formal peg.

That structure would allow China to internationalize the RMB by surrounding it with gold liquidity rather than backing it mechanically with gold. It would also allow China to compete with the dollar system at the level where the dollar is strongest: collateral.

Strategic Implication

The dollar system is a collateral system. Treasuries are not merely reserve assets. They are funding instruments, repo collateral, regulatory liquidity instruments, and balance-sheet anchors. China cannot build a rival monetary network around RMB settlement alone. It needs an asset that can perform some of those collateral functions.

The margin hikes therefore deserve attention because they may represent a preparatory step in market discipline. Before gold can be used as a broader liquidity instrument, speculative leverage must be controlled. Before the RMB can be internationalized through gold, gold pricing and gold liquidity must be internationalized through offshore infrastructure. Before gold can finance RMB liquidity, it must become repoable or collateral-eligible in practice.

The evidence does not yet support the strongest claim, namely that China has formally made gold HQLA. The evidence does support a more measured conclusion. China is creating the clearing, custody, delivery, and market-control framework needed for gold to play a larger role in offshore RMB liquidity.

The conclusion advanced by Eric Yeung and Vincent Lanci is therefore not that China is simply accumulating gold, and not that China is returning to a fixed gold standard. The conclusion is that China is building the institutional plumbing required to connect gold liquidity with RMB liquidity. If that architecture is completed, gold moves from reserve asset to collateral asset, and the RMB moves from trade-settlement currency toward financing currency.

Free Posts To Your Mailbox